Trucking insurance minimum reform is exposing underpriced road risk and changing how carriers, shippers, and investors should assess safety and cost.

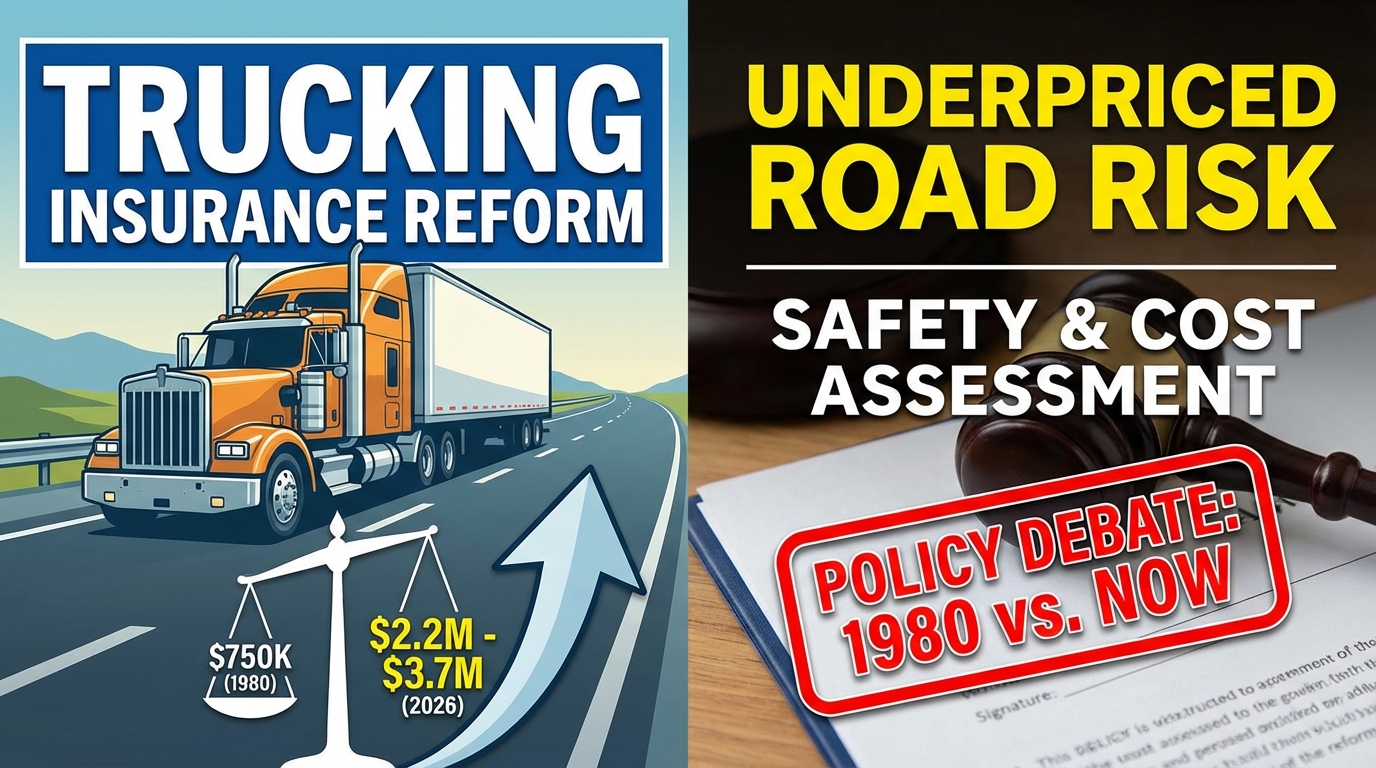

Trucking insurance minimum now sits at the center of a policy debate that is often framed as a dispute over legal inflation, but the deeper issue is capital discipline. The United States still regulates interstate for-hire trucking with a general freight liability floor set at $750,000 in 1980. That figure no longer functions as a serious risk-transfer mechanism. It functions as a political relic.

What looks like an insurance argument is in fact a structural shift in how road risk is financed. When liability floors fail to keep pace with medical inflation, the system does not become cheaper; it merely pushes more loss onto crash victims, courts, shippers, and ultimately consumer prices. The real question is not whether the threshold rises, but whether regulation forces risk to be priced before a truck is dispatched rather than after a crash is litigated.

Trucking insurance minimum is no longer a safety filter

The numbers reveal how far the market has drifted. A 2026 FMCSA Report to Congress indicates that restoring the original purchasing power of the 1980 baseline would require roughly $2.2 million using core CPI and as much as $3.7 million using medical CPI. Even the more conservative inflation lens places today’s floor far below the cost structure of a severe injury claim.

That gap matters because minimum insurance is supposed to do two things: compensate ordinary serious injury cases and impose a discipline on market entry. At $750,000, it does neither effectively. A threshold that was once designed to exclude undercapitalized operators now allows them to externalize a larger share of their risk.

This divergence exposes a fundamental tension: Washington still governs trucking with a 1980 liability floor while the claims environment reflects 2026 medicine, litigation economics, and jury psychology. The result is predictable. Safer carriers subsidize weaker ones through distorted competition, while plaintiffs pursue excess recovery through litigation because the statutory floor no longer matches real-world damages.

That is why the trucking insurance minimum should not be viewed as a narrow compliance issue. It is a market structure issue. A low floor reduces the visible cost of operating a truck, but only by shifting invisible costs elsewhere in the system.

Nuclear verdicts reflect governance failure, not just litigation inflation

The public discussion often misdiagnoses the problem by focusing exclusively on “nuclear verdicts.” That is analytically convenient and strategically misleading. The bigger verdicts are real, but they do not emerge from thin air. They emerge when juries confront evidence that a carrier failed to vet drivers, deferred maintenance, ignored hours-of-service discipline, or treated compliance as an administrative nuisance rather than an operating system.

Data from ATRI’s Trucking Litigation: A Forensic Analysis shows the scale of that shift: the median nuclear verdict reached $36 million in 2022, with awards above $10 million becoming more frequent. That figure does not mean every carrier needs $36 million in primary coverage. It means the legal system is repricing managerial negligence at levels the old insurance floor cannot begin to absorb.

The data points toward a simple conclusion: raising the trucking insurance minimum alone improves compensation adequacy, but it does not by itself improve crash prevention. A higher number creates a larger claims pool after the event. It does not guarantee that someone assessed whether the operator was a bad risk before the policy was bound.

This is where the policy debate becomes more revealing. Carriers that maintain clean inspection records, disciplined driver qualification practices, and credible maintenance programs generally have a path to higher-limit coverage that reflects their actual risk profile. The operators most threatened by higher standards are often those whose economics depend on weak underwriting and regulatory arbitrage. In other words, some opposition to reform is not really about affordability. It is about preserving access to the road for risk that has not been properly priced.

That logic should sound familiar to freight markets. When pricing fails to reflect actual cost, volume rises in the short term and fragility rises with it. Trucking is no different. Related Analysis: Negotiated Carrier Pricing and the Real Rate Gap

Why underwriting standards matter more than a headline number

The most consequential insight in this debate concerns underwriting quality. Research connecting insurance filings with carrier safety performance suggests that carriers in underwritten programs tend to show better safety outcomes than those obtaining coverage through structures with lighter front-end scrutiny. That finding shifts the debate away from a single dollar figure and toward the architecture of market access.

If a carrier can secure high-limit liability coverage through an instant-issue mechanism without serious review of crash history, out-of-service rates, maintenance practices, or BASIC performance, then a higher trucking insurance minimum may increase compensation capacity without reducing the probability of loss. Market incentives dictate that capital must screen risk before it indemnifies it.

A credible reform therefore has three moving parts. First, raise the trucking insurance minimum toward an inflation-adjusted level—whether policymakers settle near $2 million, as current proposals suggest, or move closer to the $2.2 million to $3.7 million range implied by FMCSA inflation measures. Second, require a documented federal underwriting standard before any commercial liability policy is bound. Third, tighten oversight of structures that can issue coverage with thinner solvency or underwriting discipline.

State-level movement already indicates the direction of travel. A 2025 regulatory update highlights a federal proposal to raise the liability minimum to $2 million, while New Jersey has already imposed a $1.5 million requirement for heavier commercial vehicles. Regulatory update on federal and state liability mandates That patchwork is unlikely to remain patchwork for long. Once large shippers begin integrating liability quality into procurement scorecards, underwriting discipline will migrate from regulation into commercial contracting.

The second-order effect is easy to miss. Better underwriting will not merely reshape insurance premiums; it will alter carrier consolidation. Smaller operators with strong safety records may survive and even gain share. Smaller operators relying on weak controls and thin coverage will face either recapitalization, forced compliance investment, or exit. The market will present this as a cost shock. In reality, it is a delayed correction.

[Suggested Chart: Inflation-adjusted comparison of the 1980 $750,000 liability minimum versus current equivalents under core CPI and medical CPI, alongside median nuclear verdict growth since 2015]

💡 Actionable checkpoints

For shippers, brokers, fleet owners, and investors, the policy signal is already clear:

- 💡 Audit carrier partners beyond certificate-of-insurance review; examine safety scores, out-of-service trends, and maintenance discipline.

- 💡 Reprice procurement models that still assume liability coverage is a compliance checkbox rather than a proxy for operating quality.

- 💡 For smaller carriers, document underwriting-grade safety controls now; the operators that can prove discipline will face less premium shock.

- 💡 For investors, watch underwriting reform as a consolidation catalyst in fragmented trucking segments.

- 💡 For insurers and brokers, products built around documented prospective risk assessment will likely gain regulatory and commercial advantage.

💡 Mariecon Insight

The trucking insurance minimum debate is not ultimately about a number on an insurance certificate. It is about whether the freight economy continues to tolerate underpriced road risk as a hidden subsidy. A higher threshold without underwriting reform would improve victim compensation but leave the operational hazard largely intact. A higher threshold with underwriting discipline would do something more important: it would force capital to distinguish between efficient operators and reckless ones before losses occur.

That distinction carries direct implications for B2B freight markets and the export economy. Shippers that depend on low-cost truck capacity should prepare for a phase in which some of that capacity proves uneconomic once risk is honestly priced. Freight rates may rise at the margin, but the more durable outcome is a healthier logistics base with fewer catastrophic disruptions and less legal volatility embedded in supply chains.

The likely direction over the next several years is clear. The trucking insurance minimum will move upward, either through federal legislation, state mandates, shipper procurement standards, or all three. The companies that treat this as a compliance nuisance will absorb rising cost without strategic benefit. The companies that treat it as a signal about safety governance, capital access, and carrier selection will gain a sharper advantage in a tightening risk environment.