U.S. rail carloads show an industrial freight rebound with real implications for ports, exporters, and logistics investors in 2026.

U.S. rail carloads

U.S. rail carloads are telling a story that matters far beyond the rail yard. What looks like a strong March for freight is really a clearer sign that the American goods economy is shifting from inventory repair to productive investment. That distinction matters for ports, shipowners, truckers, and exporters because investment-led freight is stickier, heavier, and far more valuable than a short-lived retail bounce.

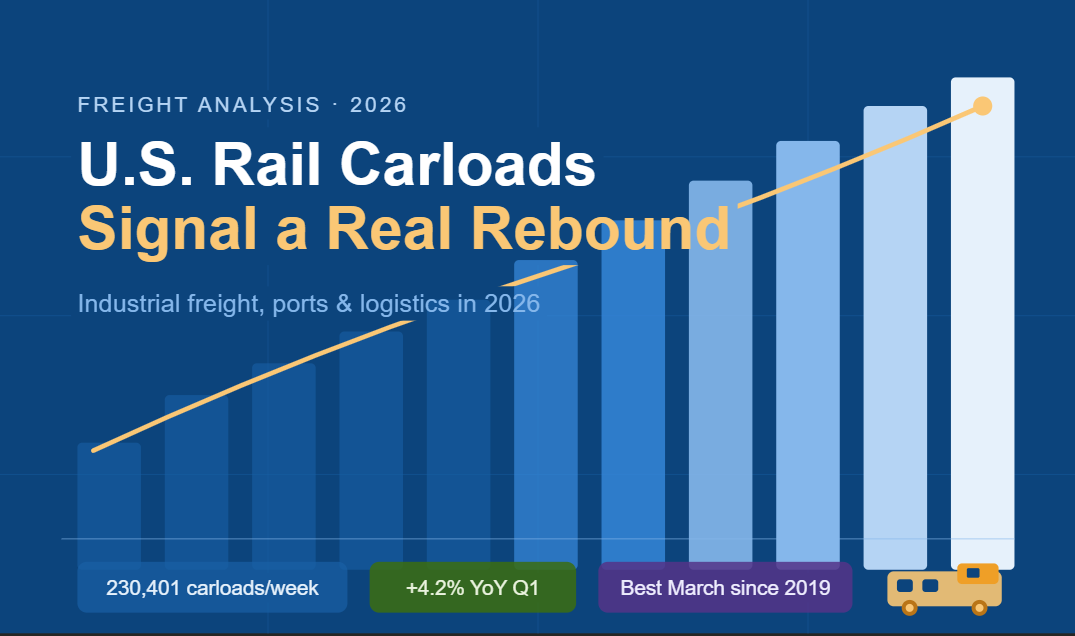

The headline numbers are strong, but the structure underneath is stronger. U.S. railroads moved an average 230,401 carloads per week in March, the best March reading since 2019, while first-quarter carloads reached 2.68 million, up 4.2% year over year, based on Association of American Railroads weekly traffic data. This is not a narrow rebound driven by one commodity. It is a broader freight reset tied to industrial inputs, chemicals, grain, and equipment-heavy demand.

For maritime readers, that is the real signal. When inland freight strengthens in chemicals, machinery, and agricultural flows at the same time, port demand does not just rise in volume. It changes in composition. Export terminals, intermodal gateways, and bulk-adjacent logistics networks start gaining leverage over pure consumer-import corridors.

Why U.S. rail carloads matter for industrial freight

Three mechanisms drive this shift. First, manufacturing is expanding again. The March 2026 ISM Manufacturing PMI report showed a PMI of 52.7%, with production at 55.1%, extending a third straight month of expansion. That matters because factory activity creates repeatable freight demand across raw materials, components, outbound finished goods, and replacement parts.

Second, chemicals are doing what they often do in early-cycle recoveries: they are revealing the underlying health of industrial production before sentiment catches up. U.S. chemical shipments averaged more than 34,000 carloads per week through March, and the category remained one of the clearest engines of rail growth. Chemicals matter because they sit upstream of everything from plastics and packaging to construction materials and industrial manufacturing.

Third, capital formation is replacing defensive supply-chain behavior. A record share of imports is now tied to capital goods rather than discretionary consumer merchandise. In plain English, companies are not just replenishing shelves. They are buying equipment to expand output. That creates a different freight map: less noise from temporary import surges, more durable flows through inland networks connected to factories, processors, and export-oriented production.

This is why rail is suddenly more informative than many ocean freight headlines. Spot container markets can move on disruption, rerouting, or blank sailings. Rail carloads, especially ex-coal, reveal whether the domestic economy is actually producing more physical goods. Investors should treat that as a harder signal.

Truck tonnage, port strategy, and export capacity

The truck market is confirming the same pattern. The ATA Truck Tonnage Index rose to 116.2 in February, up 2.6% month on month and 2.1% year on year. That is not just a trucking statistic. It suggests that committed contract freight is improving alongside rail, which reduces the odds that March was a one-off spike.

For ports and shipping companies, the implication is subtle but important. If inland industrial freight stays firm, the biggest winners may not be the gateways chasing the highest import headline volumes. They may be the nodes that connect rail, trucking, warehousing, and export processing with the least friction. The market is rewarding logistics systems that can move heavy, time-sensitive industrial cargo, not just boxes filled with consumer goods.

This also changes the risk calculus for ocean carriers and terminal operators. U.S. export competitiveness improves when domestic production rises and inland transport tightens in sync. Chemical exports, grain flows, project cargo, and machinery-related shipments all depend on reliable transfer between factory regions and port gateways. That raises the value of inland rail access, transload capacity, and berth windows that can handle less predictable but higher-margin cargo mixes.

There is a second-order effect here. As industrial freight tightens flatbed and rail capacity, logistics costs may rise faster for sectors tied to construction, machinery, and heavy manufacturing than for consumer imports. That divergence exposes a fundamental tension: reshoring and manufacturing revival may improve national production resilience, but they also create localized bottlenecks in chassis, rail slots, drayage, and specialized trucking.

What this means for supply chains and capital allocation

Executives should resist the easy narrative that stronger freight simply means stronger GDP. Freight composition matters more than freight direction. U.S. rail carloads are rising in categories that suggest a more capital-intensive economy, and that usually benefits asset owners positioned around industrial corridors rather than pure consumption hubs.

For BCOs and exporters, this is the moment to lock in inland capacity before contract conditions harden further. For terminal operators, it is a prompt to invest in rail-served handling, chemical logistics support, and faster gate coordination. For investors, the better question is not whether freight demand is improving. It is where pricing power will accumulate as industrial cargo competes for limited inland capacity.

A related read is Related Analysis: Container Shipping Disruption and the New Cost Map, especially for readers comparing inland industrial strength with volatile ocean network pricing.

✅ Actionable Checkpoints

- Prioritize exposure to logistics assets tied to industrial corridors, especially rail-served terminals and inland transload facilities.

- Review export routing for chemicals, grain, machinery, and project cargo to identify gateways with stronger rail connectivity.

- Lock in flatbed, drayage, and rail capacity early if your freight mix is linked to construction or manufacturing inputs.

- Track ex-coal rail volumes and truck tonnage together; when both rise, industrial demand is usually broadening rather than spiking temporarily.

- Stress-test supply chains for localized bottlenecks in chassis, warehouse labor, and specialized trucking before peak spring and summer demand.

💡 Mariecon Insight

U.S. rail carloads are not just signaling a better freight quarter. They are revealing a reweighting of the American economy toward production, equipment spending, and exportable industrial output. That creates opportunity for ports, carriers, and investors aligned with inland industrial networks, but it also warns that the next constraint will not be demand. It will be whether the logistics system can carry a heavier, more complex cargo mix without repricing capacity sharply upward.