Hormuz shipping crisis is reshaping LNG trade, vessel demand, and Korean shipbuilding decisions as Gulf route risk becomes a lasting cost.

Hormuz shipping crisis is no longer a temporary security shock. It now demonstrates a structural shift in how energy cargo, maritime risk, and political leverage interact across the Gulf, with consequences that extend far beyond war-risk premiums.

The immediate trigger is obvious: missile damage to Qatar’s Ras Laffan complex, new strikes on regional export infrastructure, and an effective paralysis in the Strait of Hormuz. But the deeper issue is strategic. When a chokepoint stops functioning as neutral infrastructure and starts operating as a priced political instrument, shipping markets must revalue everything from charter duration to shipyard orderbooks.

For Korean stakeholders, this matters on three fronts at once: LNG import security, tanker and gas carrier demand, and the next round of shipbuilding capital allocation. The data points toward a durable repricing of route risk rather than a brief wartime distortion.

Hormuz shipping crisis: from transit route to political tollgate

The most consequential development is not simply that traffic is disrupted. It is that Tehran appears willing to redefine passage through the Strait of Hormuz as a monetized sovereign function rather than an assumed principle of global trade. That distinction matters because freight markets can absorb danger more easily than they can absorb uncertainty over rules.

Iran’s reported consideration of transit fees or “security taxes” for commercial shipping reveals a larger contest over who captures the economic rents of maritime geography. This is not merely about military escalation; it is about converting control over a chokepoint into recurring revenue and diplomatic leverage. Once that logic enters the market, shipowners, insurers, and charterers begin pricing not just physical risk but regulatory arbitrariness.

The humanitarian dimension underscores the scale of disruption. The IMO Council safe-passage framework now centers on evacuating roughly 3,200 vessels and 20,000 seafarers stranded in the Gulf. That figure indicates that the Hormuz shipping crisis has already moved beyond insurance language and into operational immobilization.

For cargo owners, the lesson is blunt. Supply chains built on just-in-time Gulf exports assumed that maritime law and naval deterrence would preserve passage at low cost. That assumption has weakened. Buyers of LNG, crude, and refined products now face a new baseline in which route access itself becomes negotiable.

Qatar LNG disruption and the hidden freight repricing

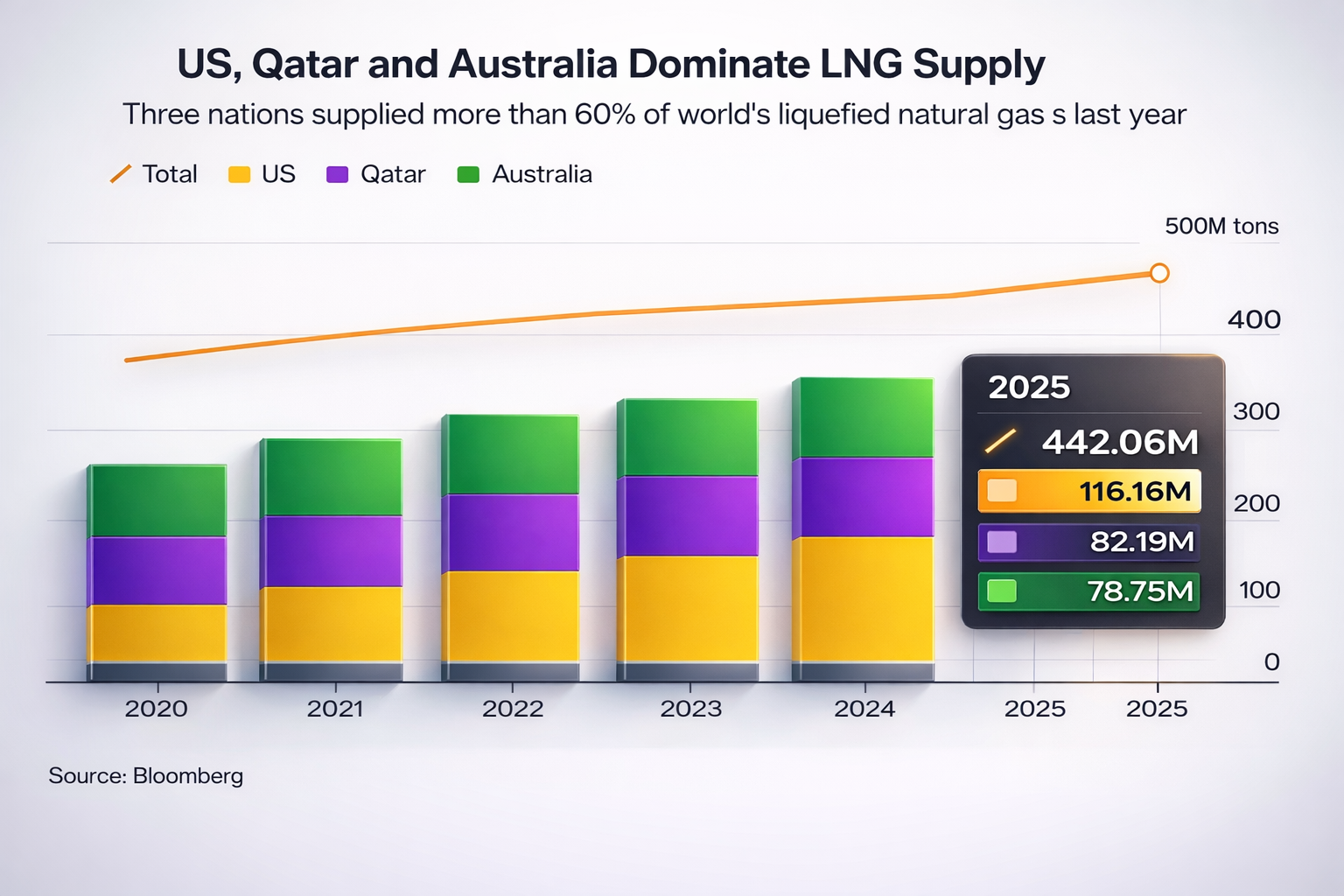

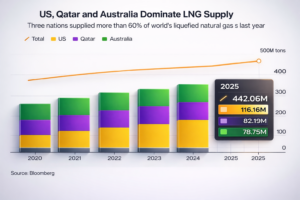

The damage to Qatar’s LNG system is not just an energy story. It is a shipping market reset. QatarEnergy has confirmed that RasGas Trains 4 and 6—equal to 12.8 mtpa—are severely damaged, removing about 17% of Ras Laffan export capacity and roughly 3% of global LNG output, with repairs estimated at three to five years, as outlined in QatarEnergy’s repair outlook.

That number appears modest at first glance. Three percent of global supply does not sound system-breaking. Yet LNG shipping does not respond linearly. It responds through route substitution, contract stress, and vessel availability. If long-term Qatari cargoes to Asia and Europe are interrupted, buyers must source replacement volumes from the US, Australia, or Africa. That raises ton-mile demand even if total LNG consumption barely changes.

This is where the Hormuz shipping crisis becomes especially relevant for Korean yards. A sustained rerouting of LNG flows supports utilization for modern gas carriers, but it also changes the ordering logic. Charterers will favor ships with stronger fuel-efficiency economics, flexible employment profiles, and financing structures that can survive volatile hire rates. The winners will not simply be builders with capacity; they will be builders aligned with balance-sheet discipline and long-duration customer relationships.

For Korean importers, the risk cuts the other way. South Korea is named among the affected long-term buyers facing force majeure exposure. That means energy security is no longer separable from fleet strategy. Utilities and trading houses may need to lock in optionality through floating storage access, medium-term charter cover, or diversified procurement beyond the Gulf. The old model—cheap supply from concentrated origins moved through assumed open sea lanes—has become strategically expensive.

What the Hormuz shipping crisis means for Korean shipping and shipbuilding

Three mechanisms drive this shift. First, war-risk pricing will remain elevated longer than many owners expect because infrastructure damage now extends the timeline beyond a ceasefire. Second, charter markets will reward flexibility, especially for LNG and tanker operators able to reposition quickly between Atlantic and Asian demand centers. Third, shipbuilding demand may rise selectively, but not evenly.

Korean yards should resist the reflexive conclusion that every disruption produces a broad newbuilding boom. That reading is too shallow. The data reveals a structural misalignment: freight volatility may increase vessel demand while financing conditions still punish speculative orders. Owners with weak charter cover will hesitate; state-backed or utility-linked buyers will move first.

The strike on Yanbu reinforces the point. Saudi Arabia had effectively used Red Sea outlets as a strategic bypass when Hormuz became unsafe. Once Yanbu itself comes under pressure, the redundancy built into Gulf export systems looks thinner than policymakers assumed. This pushes Asian buyers to re-evaluate not merely suppliers, but corridor dependence.

For Korean shipping companies, the Hormuz shipping crisis therefore creates both opportunity and exposure. Tanker and gas carrier earnings can improve under tighter vessel availability and longer average voyages. But companies with insufficient crew contingency planning, heavy spot exposure, or limited fuel-cost pass-through may find that headline rate gains conceal rising operational fragility.

For policymakers, the implication is sharper. Korea cannot treat maritime security as an abstract diplomatic issue while relying on imported hydrocarbons and export-led manufacturing. Energy procurement policy, strategic tonnage, and shipyard competitiveness now sit within the same industrial equation.

💡 3 Key Checkpoints for Korean Maritime/Shipbuilding Stakeholders

- Diversify charter and sourcing exposure: LNG buyers and shipowners should reduce concentration on Gulf-linked schedules and secure optional cargo or vessel coverage from Atlantic Basin routes.

- Prioritize financially resilient orders: Korean yards should target projects backed by long-term charters, utility demand, or export credit support rather than chasing speculative volume.

- Reprice corridor risk in procurement models: Trading houses, refiners, and logistics teams should build transit-fee, delay, and war-risk scenarios directly into contract evaluation and inventory strategy.

💡 Mariecon Insight

The Hormuz shipping crisis reveals a hard truth that Korean industry often underestimates: maritime chokepoints are not simply logistics passages; they are instruments of state power that can redraw industrial economics overnight.

If the current damage at Ras Laffan lasts even close to the projected three to five years, Korea will face a dual reality. Shipowners and yards could benefit from stronger LNG carrier and tanker fundamentals, while Korean manufacturers and utilities absorb higher embedded energy and freight costs. That divergence exposes a fundamental tension inside Korea’s export model: the nation profits from maritime volatility in one sector while paying for it across the broader industrial base.

The opportunity lies in moving earlier than competitors. Korean firms that diversify LNG procurement, secure flexible shipping capacity, and align newbuilding strategy with long-duration demand can convert the Hormuz shipping crisis into a strategic advantage. Those that treat it as a temporary Gulf disturbance will discover that the market has already repriced geography, sovereignty, and risk.